How to evaluate a gaming establishment for acquisition

An Illinois gaming establishment isn't a normal small business acquisition. The combination of a state-issued gaming license, a public-record revenue history, a regulated terminal operator agreement, and an underlying liquor license creates a specific framework that experienced IL acquirers run every deal through. This is that framework — what to verify, what to model, and what to walk away from.

The four deal types

Before the math starts, classify the deal. The risk profile changes dramatically:

- Type A — Existing gaming cafe/parlor. Gaming is the primary revenue. The license is in place, the floor is established, the revenue history is public on the state market report. Lower risk; you're essentially buying revenue continuity. Most "what's it worth?" math applies cleanly here.

- Type B — Restaurant/bar with gaming attached. Gaming is secondary. F&B is the primary business. Risk increases because you're underwriting two revenue streams that interact (foot traffic from the restaurant feeds the gaming floor, and vice versa). License is in place, but the F&B side requires its own diligence.

- Type C — Conversion target. Existing business WITHOUT gaming. You're betting that you can add a gaming license to a venue that doesn't yet have one. The state regulator's pipeline is slow and the application is non-trivial. High risk because the entire thesis depends on getting a license you don't yet have.

- Type D — Ground-up or lease-only. Vacant space. You're applying for a liquor license AND a gaming license from scratch in a municipality that may or may not approve. Highest risk; longest time-to-revenue.

Most first-time acquirers should focus on Type A or B. The license risk is removed, the revenue history is verifiable, and the model becomes a normal small-business acquisition with a regulated revenue stream.

Step 1: Pull the public state record

Before you sign an NDA, before you accept management's projections, pull the establishment's public monthly history. The state gaming regulator publishes Net Terminal Income per establishment per month, going back to 2013. This is your ground truth.

What you're looking for:

- Trend direction. Is NTI growing year-over-year? Flat? Declining? A 24-month YoY decline means something structural changed — new competition, lost regulars, lease pressure that drove the operator to under-invest.

- Seasonality consistency. Gaming is seasonal (Nov-Mar strong, Jun-Aug soft). If the seasonality is on the state record looks normal but management's projections show it ironing out, that's a red flag.

- NTI per terminal. Divide monthly NTI by the venue's VGT count (max 6 in Illinois). $4K-$5K per terminal is solid; $7K+ per terminal is excellent; $2K-$3K means the floor is underutilized and either the operator or the location is the problem.

- Recent trajectory. The last 6 months matter more than the 24-month average. A venue that did $40K NTI/month for a year and dropped to $25K NTI/month for the last 6 months is in an active decline that the seller will frame as "temporary."

Step 2: Verify the license

The gaming license is the asset. Verify:

- License number is active on the state licensee list (not just on the seller's claim)

- License is in good standing — no pending suspensions, no recent compliance violations

- License is transferable — Illinois requires re-licensing of the new owner before revenue continues. Build the gap into your model.

- Liquor license is in place and transferable — gaming licenses are tied to liquor licenses in Illinois; lose one and you lose the other

- Municipality is supportive — confirm the local board hasn't moved to restrict gaming (some IL municipalities have moratoriums; some are debating caps)

The "license check" should also include a UCC lien search — a UCC lien against the seller's gaming equipment (or the entity holding the license) can block the transfer.

Step 3: Read the Terminal Operator agreement

Illinois operators don't own the machines. A licensed Terminal Operator (TO) does. The TO contract is the single most-negotiable revenue lever in IL gaming, and the seller's contract follows the asset only if the buyer agrees to keep it.

What to verify:

- What % of NTI does the TO take? Standard is around 5%, but contracts negotiated 5+ years ago can be higher. If the seller is on a 7%-of-NTI contract and you can renegotiate to 5%, that's pure margin uplift on day one.

- Is the contract term ending? Use Agreements typically run 7-10 years. If the seller's contract has 11 months left, you have a window to switch TOs at close — material savings.

- Does the contract include exclusivity or non-compete clauses? Some TOs lock the venue into their machines for the contract duration with a penalty for early termination. Read the cancellation language carefully.

- Equipment freshness. Old machines underperform. If the TO hasn't refreshed in 3+ years, your NTI ceiling is constrained until they do.

Step 4: Lease terms

The single most-ignored deal-killer is the lease. A gaming establishment is location-dependent — moving the license requires re-licensing under a new address. So if the lease is short or the landlord is hostile to gaming, the asset has a time bomb attached.

- Remaining term + renewal options. You want at least 5+ years between current term and exhausted options. Less than 3 years is a yellow flag; less than 1 year is a red flag.

- Rent escalators. What's the increase schedule? A 3% annual escalator on a 10-year lease compounds to ~34% by year 10.

- Assignment / change-of-control rights. Can the buyer assume the lease without landlord re-approval? If the landlord can withhold consent unreasonably, you're at their mercy at close.

- Estoppel certificate. Get one from the landlord at close. It documents that the landlord acknowledges the lease, has no current disputes with the tenant, and consents to the assignment.

Step 5: Build the simple model

The math an experienced IL acquirer runs is rough but reliable:

- Trailing 12-month NTI from the public state record. Don't trust seller-supplied projections; trust the state-published numbers.

- Operator pocket = NTI × ~0.35 (after state, muni, TO splits — see the tax tier explainer)

- F&B contribution from tax returns + bank deposits, NOT seller's QuickBooks. Verify with sales tax filings.

- Operating expenses from actuals: labor (PT + manager), lease, insurance, utilities, supplies, vendor contracts. Don't accept seller's "as I run it" expense profile — model your own.

- SDE (Seller's Discretionary Earnings) = operator pocket + F&B contribution − operating expenses + add-backs (one-time costs, owner-comp normalization)

- Multiple on SDE. Solid Type A deals trade at 1.5x-2.5x SDE. Type B at slightly lower (1.5x-2.0x). Type C/D should be valued at the underlying real estate / liquor-license-only value with the gaming upside as a free option.

If the seller's ask is more than 2.5x your conservative SDE estimate, walk. The state record is publicly available, the TO contract is renegotiable, and there will be another deal. Patience is the operator's edge in this market.

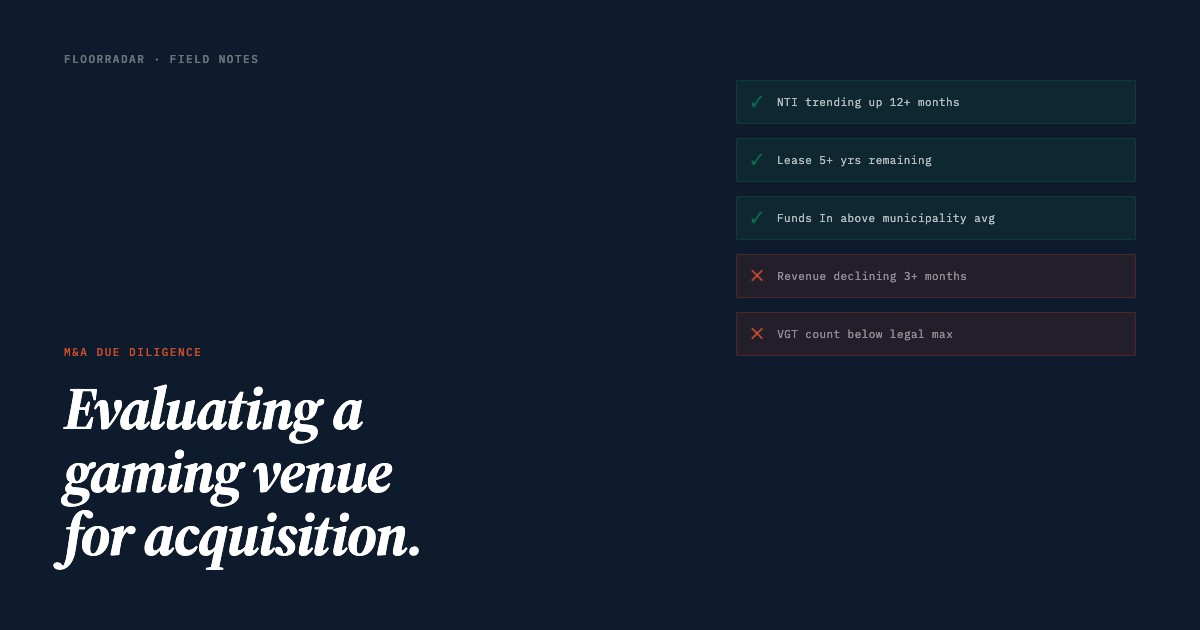

Step 6: Scorecard the deal across 8 categories

Experienced acquirers don't underwrite on revenue alone. The framework that works:

- Gaming Revenue Performance — the state regulator-record NTI trend

- Non-Gaming Revenue — F&B traction, ATM, vending

- Current Profitability — verified P&L

- Lease Terms — see step 4

- License Security — see step 2

- Competition Level — venues within 2 miles, their NTI trends

- Demographics — neighborhood income, foot traffic, evolution direction

- Transformation Potential — what could you do that the current operator isn't?

Each scored 0-10. Total of 80 maximum. 65+ = strong buy. 45-64 = conditional buy (negotiate price down). Below 45 = walk away. The conditional category is where most deals land — you find the conditional buys, fix the weak categories with the seller before close, and end up with strong-buy deals at conditional-buy prices.

The four-week due diligence sprint

Once an LOI is accepted, the clock starts. Standard IL gaming acquisition diligence runs four weeks:

- Week 1 — Deal killers. Tax returns. Bank statements. Lease document. state license verification. Liquor license verification. UCC lien search. Tax clearance certificate. Judgment search. If anything material surfaces here, kill the deal at Week 1, not Week 4.

- Week 2 — Financial verification. Detailed P&L review. Accounts payable. Payroll. Sales tax filings. Gaming revenue reconciliation. TO agreement review. Vendor contracts.

- Week 3 — Legal & compliance. Corporate documents. Certificate of good standing. All permits (health, fire, occupancy). Employee records / I-9s. Litigation check. Insurance policies. the state regulator / ILCC correspondence.

- Week 4 — Physical & close. Equipment inspection. Landlord estoppel. Final walkthrough. Inventory count. Resolve open items. Final decision: proceed or terminate.

If at any point during the sprint you discover the seller misrepresented something material, terminate. The earnest money question is real but secondary — the bigger cost is closing a deal where you don't fully trust the seller's disclosures.

The pattern most first-time acquirers miss

The seller knows their NTI. The seller knows their lease. The seller knows their TO contract. What they don't know — and what creates the buyer's edge — is the local market context. Three under-performing venues within 2 miles of the target represent acquisition pipeline beyond the current deal. A municipal moratorium being debated changes whether new licenses can enter the market. The TO's other clients in the area determine whether you can negotiate a better contract.

Operators who source deals well don't just evaluate the venue — they evaluate the venue plus the surrounding market plus the regulatory direction. The seller is selling you one establishment. You're buying a position in a market.

FloorRadar's Acquirer add-on is built around exactly this workflow — one-click market context for any IL VGT establishment, automated scorecard across the 8 categories, and the local under-performing venues identified before you even start negotiating. See the Acquirer add-on or create a free account.